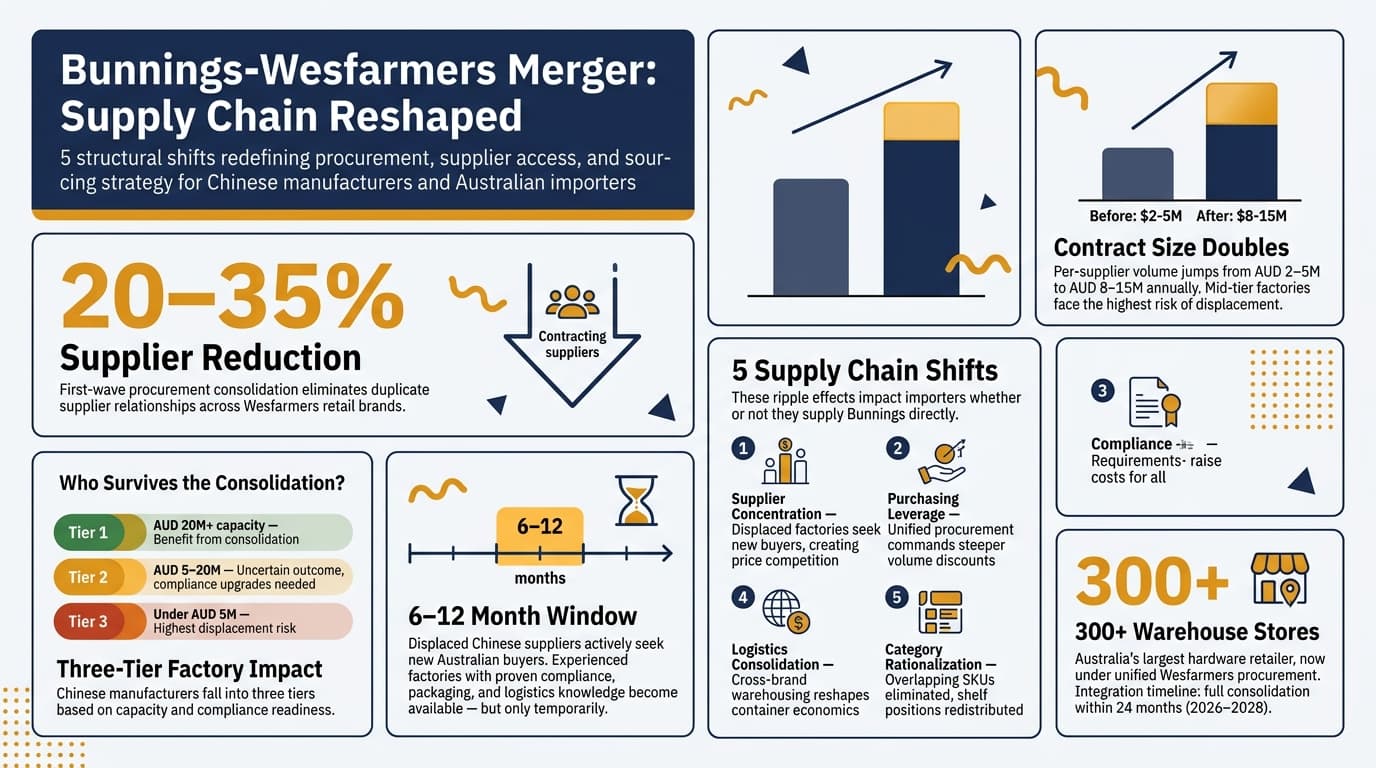

When Bunnings and Wesfarmers announced their formal merger integration in early 2026, the announcement sent ripples through supply chains extending from Melbourne distribution centers to manufacturing floors in Guangdong. The consolidation brings Australia's largest hardware retailer — operating over 300 warehouse stores nationwide — under tighter corporate integration with its parent conglomerate, and the procurement reorganization that follows will reshape how Chinese manufacturers access Australian retail shelves.

The merger is not merely a corporate restructuring story for the financial press. It represents a fundamental shift in how Australia's dominant hardware retailer sources products, manages supplier relationships, and structures procurement operations. For the thousands of Chinese manufacturers that supply products to Bunnings' shelves, and for the Australian SME importers who compete in adjacent market segments, the consolidation creates a new competitive landscape that demands strategic response.

Is your supply chain ready for retail consolidation?

Winning Adventure Global helps Australian businesses anticipate and adapt to supply chain shifts driven by retail consolidation. Our team provides strategic sourcing guidance tailored to your business.

Book a free strategy callWhat the Bunnings-Wesfarmers Integration Actually Changes

The relationship between Wesfarmers and Bunnings predates the 2026 announcement by decades. Wesfarmers acquired Bunnings in the 1990s, and Bunnings has operated as a subsidiary within the Wesfarmers portfolio throughout its expansion to market dominance. The 2026 merger integration differs from the existing ownership structure in one critical dimension: procurement and supply chain operations that previously operated with substantial autonomy are being integrated into Wesfarmers' centralized purchasing framework.

This reorganization matters because Bunnings historically maintained independent supplier relationships, separate procurement teams, and distinct sourcing strategies from other Wesfarmers retail assets. By consolidating procurement under a unified framework, Wesfarmers creates a purchasing entity with even greater leverage over suppliers — both domestic manufacturers and the international suppliers, particularly Chinese factories, that feed the Australian hardware market.

The integration timeline announced in 2026 projects full procurement consolidation within 24 months, with supplier contract transitions beginning in the second half of 2026. This timeline gives suppliers and competing importers a window to understand the changes and adjust their strategies — but the window is closing.

Centralized Procurement and Supplier Rationalization

The most immediate supply chain impact of the merger is supplier rationalization. When procurement consolidates across multiple retail brands, duplicate supplier relationships are eliminated. A Chinese factory that previously supplied similar product categories to Bunnings and another Wesfarmers retail division may find itself servicing a single, larger contract — or losing its position entirely to a competitor that wins the consolidated volume.

Centralized procurement typically reduces the supplier count by 20 to 35 percent in the first wave of integration, based on patterns observed in comparable retail consolidations across Asia-Pacific markets. The suppliers that survive rationalization receive larger contracts, while those eliminated face the difficult challenge of replacing a major customer relationship with fragmented smaller accounts.

For Chinese manufacturers, the implications extend beyond simple contract loss. Many factories have invested in production lines, packaging configurations, and compliance certifications specifically to serve Bunnings requirements. When that customer consolidates its supplier base, those dedicated investments become stranded assets unless the factory can successfully compete for the consolidated contract or find alternative buyers for the same product specifications.

Volume Thresholds and the New Supplier Economics

Consolidated procurement raises volume thresholds for suppliers. Where Bunnings previously might have maintained relationships with multiple suppliers each handling AUD 2-5 million in annual volume, the consolidated framework likely consolidates toward fewer suppliers each handling AUD 8-15 million in annual volume.

This volume concentration creates winners and losers among Chinese manufacturers. Factories with sufficient production capacity and working capital to handle larger contracts benefit from volume concentration — they receive more revenue from fewer customers, reducing sales complexity and potentially improving production efficiency through longer, uninterrupted production runs.

Factories that cannot meet the elevated volume thresholds — whether due to capacity constraints, working capital limitations, or quality consistency challenges at higher volumes — lose their position in the supply chain. These mid-tier factories, which represent a substantial portion of China's manufacturing base serving Australian retail, face the most acute risk from procurement consolidation.

What to do

Chinese manufacturers that have already diversified their Australian customer base beyond Bunnings — selling to independent hardware stores, specialty retailers, and direct-to-consumer channels — have stronger negotiating positions during supplier rationalization. Single-customer dependency on Bunnings is the largest risk factor.

Logistics Network Reorganization

The merger integration includes logistics network reorganization that affects how Chinese-manufactured goods flow into Australian retail channels. Wesfarmers operates distribution infrastructure that spans multiple retail brands, and the procurement consolidation enables cross-utilization of warehousing, transport, and inventory management systems.

For suppliers, this means goods that previously shipped to Bunnings-specific distribution centers may be routed through Wesfarmers' consolidated logistics network. The operational implications include different delivery specifications, modified packaging requirements, and potentially altered shipping schedules that affect production planning at Chinese factories.

The logistics reorganization also affects port-to-warehouse routing. Consolidated procurement volumes enable Wesfarmers to negotiate more favorable shipping terms from Chinese ports to Australian distribution centers — but those terms typically favor full-container-load shipments at regular intervals, which disadvantages smaller suppliers who cannot consistently fill containers on the required schedule.

5 Supply Chain Shifts Australian Importers Must Understand

The Bunnings-Wesfarmers merger creates five structural shifts in Australia's retail supply chain that affect importers whether or not they supply Bunnings directly. These shifts ripple through the broader sourcing ecosystem and create both threats and opportunities for Australian businesses importing from China.

| Shift | Mechanism | Timing | Importer Exposure |

|---|---|---|---|

| Supplier concentration | Procurement consolidation reduces supplier count 20-35% | 2026-2027 | High — displaced suppliers seek new buyers, creating price competition in adjacent channels |

| Purchasing leverage escalation | Unified procurement entity commands larger volume commitments and steeper discount demands | 2026-2028 | Medium — pricing pressure on manufacturers cascades to all Australian buyers as factories adjust margins |

| Compliance standardization | Integrated procurement imposes uniform quality, documentation, and audit requirements across retail brands | 2026-2027 | High — factories upgrading compliance for Bunnings-Wesfarmers may raise standards (and costs) for all Australian buyers |

| Logistics consolidation | Cross-brand warehousing and transport integration changes delivery specifications and shipping economics | 2027-2028 | Medium — shipping consolidation affects container availability and freight rates for smaller importers |

| Category rationalization | Overlapping product ranges across Wesfarmers retail brands consolidated, reducing SKU count and supplier entries | 2026-2028 | Variable — product categories with high overlap face supplier exits; niche categories may see new entry opportunities |

Shift 1: Supplier Concentration Creates Adjacent-Channel Opportunities

When large retail procurement consolidations displace suppliers, those factories do not simply cease production. They seek alternative buyers, and the Australian market — which they already understand in terms of compliance requirements, packaging standards, and logistics patterns — represents a natural target for replacement volume.

This dynamic creates price competition in channels adjacent to Bunnings. Independent hardware stores, specialty retailers, and direct-import SMEs may find Chinese suppliers offering more competitive pricing as factories compete to replace lost Bunnings volume. The opportunity exists, but it requires importers to identify these suppliers and negotiate terms while the factories are motivated to secure new business.

The window for exploiting this opportunity is relatively narrow. Displaced suppliers either find replacement buyers within 6-12 months or retrench toward domestic Chinese markets, making their Australian-market capabilities less accessible over time.

Shift 2: Purchasing Leverage Compresses Manufacturer Margins

Wesfarmers' consolidated purchasing entity commands leverage that individual retail brands could not achieve independently. Volume commitments that were previously worth AUD 50 million annually to a single brand may now represent AUD 150 million or more when aggregated across the Wesfarmers portfolio. Manufacturers negotiating against that buying power face asymmetric pressure.

The margin compression that Chinese manufacturers absorb to maintain Wesfarmers contracts does not disappear — it gets redistributed. Factories may attempt to recover margin on non-Bunnings accounts by raising prices to smaller Australian buyers. Alternatively, factories may cut costs through process changes that affect product quality. Importers who do not monitor their suppliers' financial health and pricing behavior risk absorbing costs that originate from the consolidation.

Shift 3: Compliance Standards Rise Across the Board

Integrated procurement typically involves compliance standardization — Wesfarmers imposes uniform quality management requirements, ethical sourcing standards, documentation protocols, and audit procedures across all retail brands. Chinese manufacturers that upgrade their compliance infrastructure to meet these standards create a fixed-cost base that applies to all production, not just Bunnings-Wesfarmers orders.

The result for Australian importers is that factories supplying any Wesfarmers retail brand will likely have higher-cost compliance infrastructure than factories that do not. Whether this translates to higher prices for non-Bunnings buyers depends on the factory's cost allocation decisions, but the direction of pressure is upward. Importers who source from factories with Wesfarmers contracts should understand how compliance cost allocation affects their pricing.

Sourcing Insight

Importers who source from factories without Wesfarmers contracts may benefit from lower compliance overhead — but only if those factories maintain acceptable quality standards through alternative means. Verification of factory quality systems, not just reliance on absence of major-retailer relationships, is essential.

Shift 4: Logistics Patterns Reshape Container Economics

When a purchasing entity the size of Wesfarmers consolidates shipping, the effect on container availability and freight rates extends to the broader market. Wesfarmers' shipping volumes command priority allocation from freight forwarders and shipping lines serving the China-Australia route. During peak shipping periods, smaller importers may find container space scarce or more expensive as consolidated retail volumes absorb available capacity.

The logistics reorganization also affects which Chinese ports serve as primary departure points for Australian-bound goods. If Wesfarmers concentrates its shipping through specific ports — Shanghai, Ningbo, or Shenzhen — the infrastructure and service concentration at those ports affects all shippers using those facilities. Importers who use less-congested secondary ports may find more favorable logistics conditions than those competing directly with consolidated retail volumes at primary ports.

Shift 5: Category Rationalization Redraws the Competitive Map

Retail consolidation inevitably involves SKU rationalization. Overlapping product ranges across Wesfarmers' retail brands — products that previously competed against each other on adjacent shelves in different store formats — get consolidated. The supplier that wins the consolidated listing gains volume; competitors lose their shelf position entirely.

For Australian importers, category rationalization matters because it changes which product specifications are commercially viable. If the dominant retailer consolidates around a particular specification, material grade, or packaging format, Chinese manufacturers orient production toward that specification. Importers who need different specifications — for differentiated products, higher-end segments, or specialty applications — may find fewer factories equipped to produce to their requirements as the manufacturing base concentrates around the dominant retail specification.

What Chinese Suppliers Face After the Merger

The merger's impact on Chinese manufacturers supplying Australian retail extends beyond the supplier rationalization already discussed. The structural dynamics create cascading effects that reshape the competitive landscape among Chinese factories serving the Australian market.

Chinese factories that have historically supplied Bunnings fall into three categories, each facing different post-merger dynamics. Tier-one factories — those with annual capacity exceeding AUD 20 million, strong working capital positions, and comprehensive compliance infrastructure — are best positioned to compete for consolidated contracts. These factories may actually benefit from the merger as volume concentration reduces their competitive set.

Tier-two factories — those with AUD 5-20 million in annual capacity, adequate but not exceptional balance sheets, and compliance systems that meet current Bunnings standards but may require upgrading for integrated procurement requirements — face the most uncertain outcome. These factories must invest in compliance upgrades and potentially capacity expansion to compete for consolidated contracts, without certainty that the investment will be rewarded with retained business.

Tier-three factories — smaller operations with under AUD 5 million in annual capacity, limited working capital, or compliance gaps — face the highest probability of displacement. These factories have historically survived in the Bunnings supply chain by serving niche categories, regional variations, or overflow demand that larger factories could not accommodate. Consolidated procurement reduces tolerance for multiple small suppliers, and tier-three factories are most likely to be rationalized out of the supply chain.

For Australian importers, understanding which tier their Chinese suppliers occupy provides insight into supplier stability. Importers relying on tier-three suppliers that also serve Bunnings face elevated risk of supplier disruption as those factories navigate displacement from their largest customer.

Strategic Lessons for Australian SME Importers

The Bunnings-Wesfarmers merger offers lessons for Australian businesses importing from China, regardless of whether they compete directly with Bunnings. Retail consolidation patterns repeat across sectors, and the supply chain dynamics observed in hardware retail provide a template for understanding similar consolidations in other categories.

Diversify Beyond Single-Channel Retail Dependence

The most important lesson from the merger for SME importers is the risk of single-channel dependence. Businesses whose import strategy depends heavily on supplying one major retail channel — whether Bunnings, another large retailer, or a concentrated wholesale network — face existential risk when that channel restructures its procurement.

Diversification across retail channels, direct-to-consumer sales, commercial and trade customers, and specialty segments provides resilience against procurement consolidation in any single channel. Australian businesses that built diversified customer bases before the Bunnings-Wesfarmers merger announcement have more strategic flexibility than those with concentrated retail exposure.

Diversification does not require abandoning major retail relationships — those remain valuable channels. Rather, it requires building complementary channels that provide revenue stability when large retail relationships face restructuring. For importers who have not yet diversified, the merger serves as a case study in why concentration risk matters.

If you are navigating the complexities of sourcing from China while Australian retail consolidates, understanding the fundamentals of China sourcing strategy for Australian businesses provides essential context for strategic decisions.

Build Quality and Compliance as Competitive Moats

Retail procurement consolidation raises compliance standards across the supply chain, as discussed earlier. Importers who have invested in quality management systems, compliance documentation, ethical sourcing verification, and product testing infrastructure find those investments increasingly valuable as retail buyers tighten standards.

Quality and compliance investment functions as a competitive moat in two directions. Against larger competitors who consolidate supplier bases, compliance credibility strengthens the importer's position as a reliable partner. Against smaller competitors who cannot afford compliance infrastructure, the investment creates a barrier to entry that protects market position.

The Bunnings-Wesfarmers merger signals that compliance expectations will continue rising across Australian retail. Importers who view compliance as a cost to be minimized rather than an investment in competitive positioning will find themselves disadvantaged as standards escalate.

Invest in Relationship Depth, Not Transactional Sourcing

The factories that survive procurement consolidation are those with deep, multi-year relationships characterized by joint investment, collaborative problem-solving, and mutual commitment — not purely transactional interactions driven by price comparison. Australian importers who cultivate similar relationship depth with their Chinese suppliers build supply chain stability that transactional competitors cannot replicate.

Relationship depth manifests in practical terms: joint product development, shared quality improvement programs, coordinated production planning that smooths factory capacity utilization, and transparent communication about market conditions that affect both parties. These elements create switching costs that protect supplier relationships during procurement restructuring.

Importers who treat Chinese suppliers as interchangeable vendors selected primarily on price find themselves most exposed when supply chains reorganize. Price-based supplier selection creates no loyalty, no switching costs, and no mutual commitment to work through difficult transitions together.

Is your supply chain ready for retail consolidation?

Winning Adventure Global helps Australian businesses anticipate and adapt to supply chain shifts driven by retail consolidation. Our team provides strategic sourcing guidance tailored to your business.

Book a free strategy callHow Winning Adventure Global Supports Your Supply Chain Strategy

The Bunnings-Wesfarmers merger represents a specific event in one retail sector, but the underlying dynamics — procurement consolidation, supplier rationalization, compliance escalation, and logistics reorganization — repeat across Australian retail categories. Businesses that understand these patterns and build supply chain strategies accordingly position themselves for resilience regardless of which sector experiences the next consolidation.

Winning Adventure Global provides Australian businesses with the China sourcing expertise, supplier relationship management capability, and strategic guidance needed to navigate these dynamics. Our team works alongside importers to build diversified, resilient supply chains that withstand retail consolidation, compliance escalation, and the broader structural changes reshaping Australia-China trade.

Whether you need to diversify your supplier base, upgrade quality and compliance systems, or develop strategic supplier relationships that survive procurement restructuring, our Australia-based and China-based teams provide practical guidance informed by direct experience across both markets.

Frequently Asked Questions

Will the Bunnings-Wesfarmers merger reduce the number of Chinese suppliers serving the Australian hardware market?

Yes, supplier rationalization following procurement consolidation will likely reduce the number of Chinese factories directly supplying Bunnings-Wesfarmers by an estimated 20 to 35 percent during the integration period spanning 2026 to 2028. However, this reduction affects only the Bunnings-Wesfarmers supply chain specifically. Chinese suppliers displaced from that channel typically seek alternative Australian buyers, meaning total Chinese manufacturing capacity serving the Australian hardware market may not decrease proportionally. The supply base redistributes rather than simply contracts. Importers who actively monitor the supplier landscape can identify factories with proven Australian-market capability that become available as the rationalization proceeds.

How should Australian SME importers adjust their sourcing strategy following the merger?

SME importers should pursue three adjustments. First, conduct a supplier concentration audit to identify whether any of your Chinese factories have significant Bunnings-Wesfarmers exposure — those suppliers face elevated disruption risk during procurement consolidation. Second, accelerate customer channel diversification to reduce your own exposure to any single Australian retail channel undergoing restructuring. Third, invest in supplier relationship depth — joint planning, shared quality improvement, and transparent communication — that creates switching costs and mutual commitment insulating your supply chain from procurement reorganizations. The specific priority among these adjustments depends on your current supplier portfolio, customer concentration, and product category exposure to retail consolidation dynamics.

Does the Bunnings-Wesfarmers merger create opportunities for smaller importers?

Yes, the merger creates specific opportunities. Supplier displacement from Bunnings-Wesfarmers procurement consolidation releases experienced Chinese manufacturers into the broader Australian market. These factories understand Australian compliance requirements, packaging standards, and logistics patterns — knowledge that typically takes years to develop — and they actively seek replacement volume. Importers who engage these factories during the 6-12 month window when they are most motivated to secure new Australian business can negotiate favorable terms. Additionally, category rationalization may eliminate product specifications from Bunnings shelves that independent retailers can fill, creating demand for importers who can source those displaced product categories from alternative Chinese suppliers.

What product categories face the most supply chain disruption from the merger?

Product categories with high overlap between Bunnings and other Wesfarmers retail brands face the most disruption from SKU rationalization and supplier consolidation. Hardware and fastenings, timber and building materials, paints and coatings, garden products, and electrical supplies all have substantial overlap across Wesfarmers retail formats and are likely to experience consolidation pressure. Categories with less overlap — specialty building products, professional trade equipment, and regionally specific materials — face less disruption. Categories where Bunnings has historically maintained multiple suppliers for the same product specification face the greatest supplier count reduction, while categories with few qualified suppliers may see minimal change.

How can I tell if my Chinese supplier is at risk from the merger before disruption occurs?

Three indicators help assess supplier risk. First, ask your supplier directly about their Bunnings-Wesfarmers exposure — what percentage of annual revenue comes from those channels, and whether they have received communication about contract consolidation or restructuring. Second, evaluate whether your supplier has the financial resources to invest in compliance upgrades and potentially capacity expansion that consolidated procurement may require, or whether they operate at a scale and margin level that makes such investment difficult. Third, assess whether your supplier has diversified their buyer base beyond Wesfarmers retail brands — factories with multiple Australian customers across different channels have stronger negotiating positions and lower disruption risk than single-customer-dependent operations. If all three indicators point toward vulnerability, developing alternative supplier relationships before disruption occurs is prudent.

China Sourcing Strategy

Is your supply chain ready for retail consolidation?

Winning Adventure Global helps Australian businesses anticipate and adapt to supply chain shifts driven by retail consolidation. Our team provides strategic sourcing guidance tailored to your business.

Book a free strategy callFree initial consultation · We respond within 4 business hours